Step by Step Instructions to Complete IRS Form W-8BEN: A Plain-Language Guide for Foreign Remote Workers Without a U.S. Tax ID

Why This Form Matters to You

If you live outside the United States and provide services remotely to a U.S. company, you have almost certainly been asked to complete Form W-8BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals). Many foreign contractors panic when they see "IRS" at the top of the page. There is no need to worry.

Form W-8BEN is not a tax return. It does not, by itself, create a tax bill. It is a certificate—a signed statement that tells the U.S. company three simple things:

- You are not a U.S. person.

- You are the true owner of the money being paid to you.

- If a tax treaty applies, you may qualify for a reduced tax rate or exemption.

The legal foundation for this form comes from Internal Revenue Code (IRC) §§ 1441 and 1442 and the related Treasury Regulations. Under these rules, U.S. payers must generally withhold 30% of certain U.S.-source payments to foreign persons (see IRC § 1441(a)). When you provide a properly completed Form W-8BEN, the company has documentation showing you are foreign, which protects both you and the company.

A critical point for remote workers: under the source-of-income rules in IRC § 861 and § 862, income from personal services is sourced to the place where the work is physically performed. If you perform all of your work outside the United States, that income is generally foreign-source income and is not subject to the 30% U.S. withholding tax. Companies still request the W-8BEN to confirm your foreign status and to avoid backup withholding under IRC § 3406.

In short: this form is your friend. It is the document that keeps the U.S. government from automatically taking nearly a third of your pay.

The Good News About Not Having an SSN or ITIN

A common fear is: "I don't have a U.S. tax ID number. Can I even complete this form?"

Yes, you can. This is one of the most important things to understand. The official Instructions for Form W-8BEN (Rev. October 2021) make clear that a U.S. taxpayer identification number is not always required. The instructions explain that you must provide an SSN or ITIN only in limited situations—for example, if you are claiming certain treaty benefits that have no exception, or if you are a partner in a partnership conducting a U.S. trade or business.

For most remote contractors simply documenting foreign status, you can leave the U.S. tax ID line blank and instead provide your foreign tax identifying number from your home country. We will walk through exactly how to do this below.

Before You Start: Make Sure W-8BEN Is the Right Form

The form itself lists situations where you should use a different form. Read these carefully:

- You are not an individual (you are a company or entity) → use Form W-8BEN-E.

- You are a U.S. citizen or resident alien → use Form W-9.

- Your income is effectively connected with a U.S. trade or business → use Form W-8ECI.

- You are physically performing services inside the United States → you may need Form 8233 or Form W-4 instead.

For the typical foreign national working remotely from their home country for a U.S. client, Form W-8BEN is correct.

One more eligibility check: you must qualify as a nonresident alien. The instructions explain that you are a nonresident alien if you do not meet the "green card test" or the "substantial presence test." Publication 519 describes the substantial presence test in detail (generally, being physically present in the U.S. for 183 days under a weighted three-year formula). If you live abroad and rarely or never visit the U.S., you are a nonresident alien.

Walking Through the Form, Line by Line

The form has three parts. Let's translate each line into plain English.

Part I — Identification of Beneficial Owner

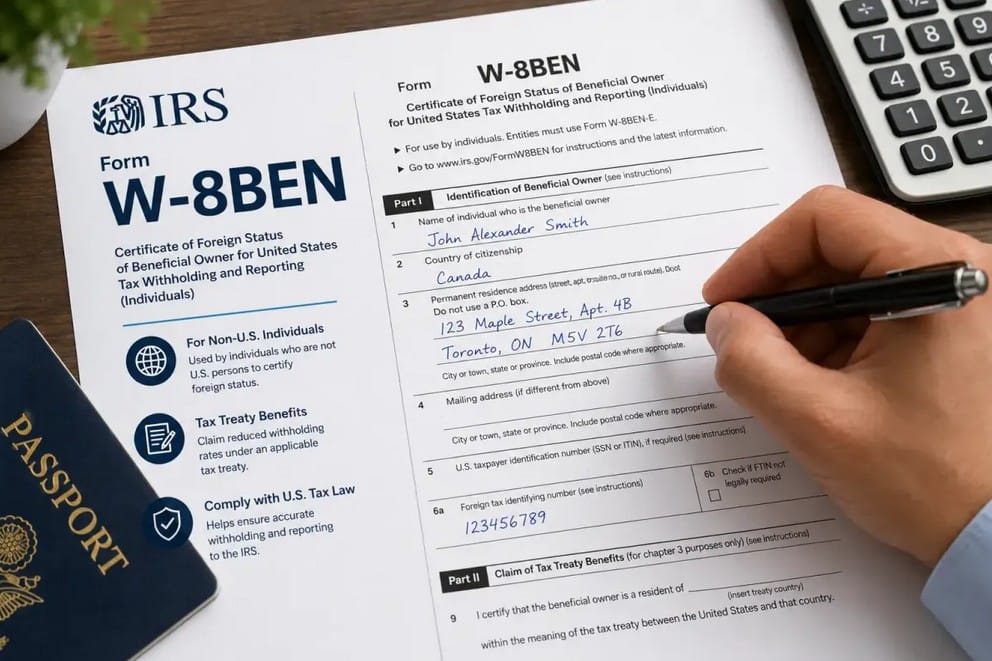

Line 1 — Name of individual who is the beneficial owner. Write your full legal name, exactly as it appears on your passport. "Beneficial owner" is just legal language meaning the real person who owns and receives the income. That is you.

Line 2 — Country of citizenship. Enter the country where you are a citizen. The instructions explain that if you hold dual citizenship, enter the country where you are both a citizen and a resident at the time you complete the form. If you are not a resident in any country where you hold citizenship, enter the country where you most recently lived.

Line 3 — Permanent residence address. This is the address in the country where you pay (or would pay) income tax as a resident. The instructions are strict here: do not use a P.O. box, do not use an "in-care-of" address, and do not use the address of a bank or financial institution. Use your actual home address. If your country does not use street addresses, the instructions allow you to write a descriptive address that accurately shows where you live.

This line matters enormously. If you write a U.S. address here, you may trigger questions about whether you are really a U.S. resident, which could cause withholding.

Line 4 — Mailing address. Complete this only if your mailing address is different from the address on Line 3. If they are the same, leave it blank.

Line 5 — U.S. taxpayer identification number (SSN or ITIN), if required. Here is the line that worries people most. Notice the words "if required."

If you do not have an SSN or ITIN, and you are not in one of the special situations described in the instructions (such as claiming a treaty benefit that requires a U.S. number, or being a partner in a U.S. partnership), you may leave this line blank. For most remote contractors documenting foreign status and providing a foreign tax number on Line 6a, Line 5 stays empty.

Line 6a — Foreign tax identifying number (FTIN). This is where you write the tax ID number issued by your own country—the number your home government uses to identify you as a taxpayer. Examples include a national tax number, a fiscal code, or a tax registration number.

The instructions explain that if you hold an account with a U.S. financial institution and receive certain U.S.-source income reported on Form 1042-S, you generally must provide your FTIN here—unless an exception applies. Providing your FTIN on Line 6a also lets you claim treaty benefits without needing a U.S. ITIN in many cases. This is exactly why the foreign tax number is so valuable to you.

Line 6b — Check if FTIN not legally required. This box was added in the October 2021 revision. Check it only if your country does not issue tax ID numbers, or you are genuinely not required by your country's law to have one. If your country issues you a tax number, do not check this box—just put your number on Line 6a. The instructions allow you to add a brief written explanation in the margin if you check this box.

Line 7 — Reference number(s). This is optional. The instructions say it may be used for any referencing information helpful to the company, such as an account number or a contractor ID. Many people leave it blank. If your U.S. client asks you to include a vendor number, put it here.

Line 8 — Date of birth (MM-DD-YYYY). Enter your date of birth in the U.S. format: month, then day, then year. The instructions give a clear example—someone born on April 15, 1956, would write 04-15-1956. This is required if you hold an account with a U.S. financial institution.

Part II — Claim of Tax Treaty Benefits

This section is only for people claiming benefits under an income tax treaty between the United States and their country. The United States has treaties with many—but not all—countries.

Important for remote workers: If you perform all of your work outside the United States, your service income is foreign-source and is generally not subject to U.S. tax at all. In that situation, you usually do not need to complete Part II, because there is no U.S. tax to reduce. Part II becomes relevant when you receive U.S.-source income such as royalties, certain dividends, or interest.

Line 9 — Country of residence for treaty purposes. If you are claiming a treaty benefit, write the country where you are a tax resident under the terms of that treaty. The instructions stress that you must be a resident of that country "under the terms of the treaty." A list of U.S. tax treaties is available at IRS.gov.

Line 10 — Special rates and conditions. The instructions are clear that Line 10 is used only in specific situations not already covered by Line 9. For example, you complete Line 10 if:

- You are a student or researcher claiming a treaty exemption on scholarship income.

- You are claiming a special royalty rate.

- You are claiming benefits on business profits or gains not attributable to a permanent establishment.

- You are claiming benefits under a treaty's remittance-based provision.

Most ordinary remote service contractors leave Line 10 blank. If you do use it, you must name the specific treaty article, the paragraph, the withholding rate, and the type of income, and then explain in plain words why you qualify.

If you are unsure whether a treaty benefit applies to you, this is precisely the moment to consult a qualified tax professional.

Part III — Certification

This is the legal heart of the form. By signing, you are declaring under penalties of perjury that everything you wrote is true, correct, and complete. The signature confirms, among other things, that:

- You are the beneficial owner of the income.

- The person on Line 1 is not a U.S. person.

- You are a resident of any treaty country you listed.

Signature. Sign the form. The instructions explain that the form may also be signed electronically, but a valid electronic signature must show that the form was electronically signed by an authorized person (for example, with a time-and-date stamp). The instructions specifically warn that simply typing your name into the signature line is not, by itself, a valid electronic signature unless the system meets the regulatory requirements.

Date (MM-DD-YYYY). Use the U.S. date format again.

Print name of signer. Write your name in print.

There is also a checkbox certifying that you have the capacity to sign for the person on Line 1. If you are signing for yourself, check it.

What to Do After You Sign

Do not mail this form to the IRS. This surprises many people. The instructions are explicit: give the completed form to the withholding agent or payer—that is, the U.S. company paying you. The company keeps it in its records as proof of your foreign status.

How Long the Form Lasts

A Form W-8BEN is generally valid from the date you sign it through the end of the third following calendar year, unless your information changes. The instructions give a helpful example: a form signed on September 30, 2015, remained valid through December 31, 2018.

If anything changes—your address, your citizenship, your residency, or especially if you become a U.S. person—you must notify the company and submit a new form within 30 days. Moving to the United States is specifically treated as a "change in circumstances" that ends your right to claim treaty benefits and may require you to file Form W-9 instead.

Common Mistakes to Avoid

- Leaving Line 6a blank when you have a foreign tax number. Your FTIN is what lets you skip the U.S. ITIN. Use it.

- Writing a U.S. or P.O. box address on Line 3. This can trigger withholding and questions about your status.

- Claiming treaty benefits you don't qualify for. Only complete Part II if you are genuinely a treaty-country resident and the income is U.S.-source.

- Using an outdated form. Always download the current revision from IRS.gov/FormW8BEN.

- Forgetting to sign and date. An unsigned form is invalid.

Final Thoughts

For a foreign national working remotely for a U.S. company, Form W-8BEN is a straightforward and protective document. You can complete it confidently even without a U.S. Social Security Number or ITIN—your home-country tax number on Line 6a usually does the job. Accuracy and honesty are essential, because you are signing under penalties of perjury.

If your situation involves U.S.-source income, treaty claims, time physically spent in the United States, or any uncertainty about your residency status, do not guess.

Disclaimer: This article is provided for informational and educational purposes only. It does not constitute legal, accounting, or professional tax advice. Tax situations vary, and you should consult a qualified tax professional regarding your specific circumstances. For your safety, do not share sensitive personal information such as Social Security Numbers, tax ID numbers, or specific financial figures in any online conversation.